Mountains on mountains: Reeves at Davos and Trump, McKinley, and Tariffs

What I wrote this week

Hello,

Thanks for coming by. Since this is my first post here, I’m starting with a brief bit of navel-gazing about what this Substack will be before I get to anything substantive. Feel free to scroll past the next few paragraphs if that sounds dull.

I’ve been looking for a midpoint between Twitter/X and full Economist articles to share some of what I’ve been working on and thinking about. I’m hoping this Substack will help fill that niche. Largely, I’m running it for pretty selfish reasons—putting rough thoughts on paper tends to clear them up, and doing so in public lets others (ideally productively) respond.

But, hopefully there’s also some value for others in a stream of somewhat-thought-through takes on the British economy and governance, monetary policy, the bond market, growth, and other miscellany. Ideally, at a minimum, there should be a steady supply of interesting provocations (and charts).

If any of that sounds of interest, then do hit the red button down here:

And I’m very much still playing around with the format, so let me know what does and doesn’t add value for you.

Between Davos and Denali, there’s been something of an inadvertent alpine theme to my writing over the past week. On Wednesday, I helped dissect our Editor’s chat at Davos with Britain’s seemingly-no-longer-press-shy chancellor: The Rachel Reeves theory of growth.

Britain, she says, faces “a long-standing supply-side issue”. Demand is not the problem, but “there are too many things holding back investment”. What is needed is “an active supply-side approach, to improve the productive capacity of our country”. By that logic, the government’s job is to remove barriers to investment, making space for the private sector to direct capital to productive uses. That emphasis on deregulation marks a shift for Ms Reeves, who in opposition took inspiration from Bidenomics—a more heavy-handed approach where private investment is guided, and sometimes subsidised, by the state.

Having spent more time than I care to admit reading Reeves-related economics takes, three main things struck me from the conversation.

As the quote above gets to, the chancellor was sounding awfully deregulatory. The central fact of her growth thesis is that Britain under-invests. The 2022/3-era Reeves answer to that problem, I think, would have been to talk about ‘crowding-in’, state-directed investment, taking inspiration from Biden, and so on. Now, she seems mostly to be saying that her job is to help the state get out of its own way (good!). As to whether that reflects a genuine shift in belief, Britain’s lack of fiscal space to splash cash on market-shaping, Bidenomics’ political failure in the US, or something else, your guess is as good as mine.

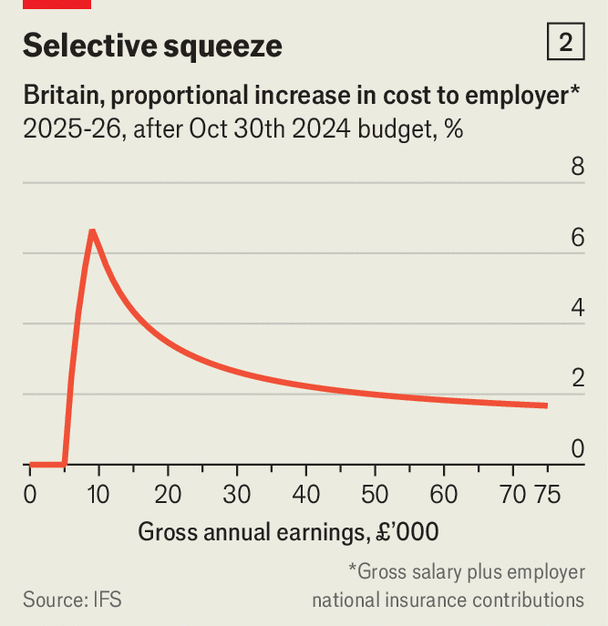

We pushed Reeves on what, to me, was the most curious part of her budget: the choice to push a disproportionate share of the employer’s national insurance rise onto lower-paid jobs. The chart below from the piece illustrates that. She denied that anything was afoot here, and said she just needed the money.

Up to you whether to believe that denial (I have my doubts…)—but the conversation points, potentially, to a more interesting arm of her pro-investment agenda than the standard YIMBY fare: actively penalising employers and sectors that use lots of low-wage workers, rather than investing more in human or physical capital. “The e-checkout chancellor”, perhaps?

And there was a striking gulf between the boldness and ambition of the chancellor’s tone, versus the policies that she’s actually delivered so far: not much boldness in the October Budget, a bit in the pro-housebuilding and pro-infrastructure agenda—but partly because recent governments have set the bar so low there. But, she insists, she is genuinely totally single-minded in her pursuit of growth. The ‘bull case’ is that this presages more ambition going forward (there’s still 90% of this parliament to go, and that Labour majority is large); the ‘bear case’ is that there’s a mismatch between what the chancellor thinks will be enough to move the dial on British growth and what Britain’s bleak reality actually demands. Best hope it’s the former.

And earlier in the week, I wrote our Free Exchange column, working through the murky political-economic debate on Trump’s tariff plans: Do tariffs raise inflation?

Mountain-naming turned out to be a curiously high priority for Donald Trump. Mere hours after his inauguration, the president signed an executive order to change the name of America’s highest peak from Denali, of indigenous Alaskan origin, back to Mount McKinley, as it was officially known until Barack Obama intervened in 2015. The rechristening reflects more than just the usual culture-war ping-pong. Like Mr Trump, William McKinley was a “tariff man”. As a congressman and later president, he swung America toward protectionism in the late 19th century. “President McKinley made our country very rich through tariffs and through talent,” said Mr Trump in his inaugural address.

Pro-free-trade arguments would not, I suspected, be vastly new to Economist readers, but the current tariff debate in the US has a few interesting wrinkles that I wanted to pull out. For one, it’s heavily shaped by the dominance of inflation as voters’ main economic worry. So most of the anti-tariff messaging from the Democrats has involved arguing that tariffs are inflationary. I suspect that sort of argument polls excellently, and there’s certainly a germ of truth to it (tariffs do very much raise the prices of the goods affected).

But, as John Cochrane wrote about at great length, it’s also a little frustrating given the reason to object to tariffs really isn’t that they’ll kick off sustained broad-based inflation—they should just be a one-off shift to the price level, and only for imported goods (they may well be offsettingly disinflationary to home-produced goods if households’ spending power is soaked up in higher prices).

The bigger issue, as I get to towards the end of the column, is how tariffs misallocate resources, and, over time, reduce productivity by hindering competition and access to international markets. Harder, perhaps, to get all that on a bumper sticker though.

Separately, it’s really notable how much the best pro-tariff arguments hinge substantially on other countries not retaliating. That’s certainly true vis-a-vis the argument that dollar appreciation will offset the impact of tariffs, as I work through in the column— but applies more generally as well.

More to say on all this, I’m sure, whenever any actual new tariffs start flowing through.

What I’m thinking about

What are some AI ‘canaries in the coalmine’ for knowledge work? Hard to argue, I think, that large swathes of white-collar ‘email jobs’ won’t be done pretty effectively by AI in the fairly near future—though Claude/o1’s poor pun game gives me some hope for my own future employment prospects. But for the moment, my London lawyer friends assure me there’s still a pretty tight labour market for junior corporate lawyers, which is a job that has seemed plausibly-automatable since even before LLMs took off. I’m very interested in ideas on where to look for barometers to assess how fast and far-reaching the automation cycle will be.

Is Britain too exposed to the global financial/liquidity cycle? The way that US political-economic conditions yanked up bond yields around the world in over the past few months, and particularly in Britain, is exactly the sort of thing that a regime of floating exchange rates ought in theory to prevent. Clearly, that’s not happened. Is it possible or desirable for policy to blunt a country’s exposure to shifts in global liquidity? (I’ve been enjoying reading some of Hélène Rey’s work on the global financial cycle over the past day or two.)

What are the best arguments against nuclear power in Britain today? One thing I’m planning to spend more time thinking about over the next few months is Britain’s energy market. The case that Britain will pretty desperately need a lot more baseload power if there’s any chance of phasing out gas (there is only so far demand variability and energy imports can get you in terms of dealing with intermittency) feels hard to argue with. Ditto, I struggle to see many viable alternatives beyond nuclear. But before I become a total bore on this topic, I do want to make sure I’m getting the best version of the case for the other side—since, demonstrably, the political enthusiasm to kick off new nuclear projects in Britain at the moment doesn’t feel vast.

The best things I’ve read recently

A User's Guide To Structuring The Global Trading System — Stephen Miran

An valiant attempt to reconcile Trumpist intuitions with mainstream economics from Trump’s new top economics adviser. Put out in November, but something worth referring back to as we see what Trump II policies look like in practice. (I don’t agree with most of it, but the push for coherence is admirable.)

Broadly, there were two interesting ideas in Miran’s report. First: dollar appreciation blunts the impact of tariffs, which I spent a while working through in this week’s Free Exchange. (Most important point there: that logic doesn’t hold if, as looks overwhelmingly likely, tariffs spawn retaliation).

Second and much wider-reaching: an inversion of the conventional logic of exorbitant privilege—the benefits to the US of the dollar’s status as a global reserve currency. That status, Miran argues, is not a perk but a burden: the costs, in terms of an overvalued dollar, outweigh the benefits (typically: the ability for the government to borrow more cheaply because of strong foreign demand for Treasuries). And, he says, the situation is worsening.

As the United States shrinks relative to global GDP, the current account or fiscal deficit it must run to fund global trade and savings pools grows larger as a share of the domestic economy. Therefore, as the rest of the world grows, the consequences for our own export sectors—an overvalued dollar incentivizing imports—become more difficult to bear, and the pain inflicted on that portion of the economy increases.

Eventually (in theory), a Triffin “tipping point” is reached at which such deficits grow large enough to induce credit risk in the reserve asset. The reserve country may lose reserve status, ushering in a wave of global instability, and this is referred to as the Triffin “dilemma.” Indeed, the paradox of being a reserve currency is that it leads to permanent twin deficits, which in turn lead over time to an unsustainable accumulation of public and foreign debt that eventually undermines the safety and reserve currency status of such large debtor economy.

My own view is that complaining about too many foreigners wanting to buy US government debt at a time when deficits are already 6-8% is—to put it politely—cheeky, and that America should shut up and enjoy the lower borrowing costs. But the driving force behind US economic policy over the next four years is going to be taking a rather different attitude…

Grasping For Growth — Ben Ansell

A walkthrough of the political-economic “theories of growth” different British governments have followed. Ansell worries, as I do to an extent, that this government’s not quite figured its own out yet.

Which leads us to the crux of the matter. Labour’s current plans on their own will not get them re-elected because there are minimal gains for most and tax rises, which even if disguised, are still likely to have contractionary effects. For the plans to work politically, they have to work economically, which means they need to create a framework for sustained economic growth by 2029.

But Labour does not seem to have a coherent theory of how that growth might emerge. Worse, the current agenda is a mishmash of different theories of growth that potentially offset one another.

Where I’d part from Ansell’s analysis, potentially, is that I think I can see a rough synthesis that Labour is (inelegantly) grasping towards: a bolting together of left-YIMBYism and classic Labour tax-and-spend.

Lots of unknowns, still, and the coherence is perhaps more in the rhetoric yet than the policy programme, but it doesn’t feel totally absent either. Unhelpfully for the economics pundit, all the ‘securonomics’ talk from opposition that supposedly defined Reeves’s growth philosophy seems to have turned out to be a total distraction.

Inside the Houthis’ moneymaking machine — The Economist (Corbin Duncan)

Great piece by one of my colleagues on how the Houthi control of a Red Sea chokepoint has turned into a stunningly sophisticated marine highwayman operation. Stationary bandits, but at sea.

IT’S A REALLY, surprisingly user-friendly experience,” says Stephen Askins, a shipping lawyer, of his interactions with the Houthis, the militia that has been attacking commercial ships in the Red Sea for more than a year. “You write to them, respectfully. They write back, respectfully, and wish you a happy passage.”

Not everyone is greeted cordially. In 2024 the Houthis took aim at almost 200 vessels, damaging more than 40, and attacks have continued into 2025. With Iranian weapons and Russian intelligence, the Yemeni rebels partly control what enters Bab al-Mandab, at the mouth of the Red Sea, and thus the Suez Canal through which 12% of world trade normally flows. Not since the second world war have merchant ships faced such peril.

Heathrow Expansion: Britain’s Runway to Growth — UK Day One

An exhaustive walkthrough of the case for expanding Heathrow that goes point-by-point through pretty much every objection. I particularly enjoyed the thinking on the economics of hub airports.

The economic case for a hub airport is distinct from that of other airports. Specifically, hub airports demonstrate increasing returns to scale. For every additional Heathrow connection, the value of other connections rises, as more potential passengers can be captured. Suppose Heathrow adds a direct flight to Chongqing, a city of 30 million in central China. This benefits anyone in or around Chongqing who wishes to fly to London, for work, tourism or study, but also benefits anyone who wants to connect to a European, North American or North African airport which is served by Heathrow. Furthermore, anyone living in the UK or Europe now has an additional way to get to Chongqing. The route becomes more valuable for each additional available route. Note that this logic applies not just by adding more long haul routes to places like Chongqing, but also by adding smaller short-haul destinations in the UK and Europe.

Why UK gilt yields have risen since the US election and what the government might do — Sushil Wadhwani

A thoughtful column from an ex-MPC member on why gilt yields went up, and what the government can do to lessen the intensity of spillovers to the UK from global economic volatility. As a card-carrying inflation-linked bond fan, I especially liked this one:

Take measures to reduce the debt interest bill directly – for example, I have previously proposed allowing the Bank of England to set its own inflation target (Wadhwani 2024). A key point to make here is that the markets confront Knightian uncertainty with regards to what future UK governments will look like in, say, 15 years. Anything that makes it more difficult to amend the inflation target would be perceived as a good thing by markets. I also suggested that the proportion of issuance taking the form of index-linked debt be increased – this would be seen as a signal that the UK government believes that the inflation target will be hit. Note that these measures would reduce the ‘inflation risk premium’ that the UK government currently pays unnecessarily, and, as I showed above, would make the fiscal arithmetic look less forbidding.

And, to close out, a few of my favourite charts at the moment

The last round of Trump tariffs very visibly raised domestic prices for the goods they affected (via Goldman Sachs)

Even when you look past the impact of a strong dollar, sterling has fallen noticeably in 2025. A less-than-ideal backdrop to the British government’s current attempt at an international charm offensive. White line: GBP Real Exchange Rate vs Trade-Weighted Basket, Blue line: GBP vs EUR (my chart, data from Bloomberg).

And, lastly, a moment of silence for Britain’s Q1 2024 growth spurt. We won’t forget you… (via Resolution Foundation)

Don’t forget, some of the inflation risk premium in the UK is structural as demand from defined benefit pension schemes and (increasingly) insurers who are taking on those liabilities.