Britain's AI bear case

A handful of troublingly plausible ways the next decade could not go Britain's way

There’s an entirely respectable career to be made in conjuring up prophecies of economic doom for Britain. The past few years have offered plenty of raw material. Still, that’s a temptation I mostly prefer to resist. Permit me, though, a brief exception—a moment to indulge my inner perma-bear. I think it’s worth the lapse.

I want to air a possibility that has been troubling me for the past year1: that Britain could make a real mess of the AI age. Certainly, there are plenty of great AI-adjacent British institutions, like AISI2, ARIA, Arm and (further into the alphabet) DeepMind. But that does not, alone, mean that Britain’s wider economy, or its political system, is well-placed to navigate the shocks coming. On the contrary, I worry that Britain is especially exposed.

Here are a few scenarios. They almost certainly won’t all happen, and aren’t even always entirely mutually consistent. But, hopefully, the exercise pulls open a few windows into how the coming years could go wrong for Britain. (A common starting-point isn’t quite AI doom or rapid takeoff, but a case where much of the economy does get remade rather quickly.)

1. First, AI kills the lawyers

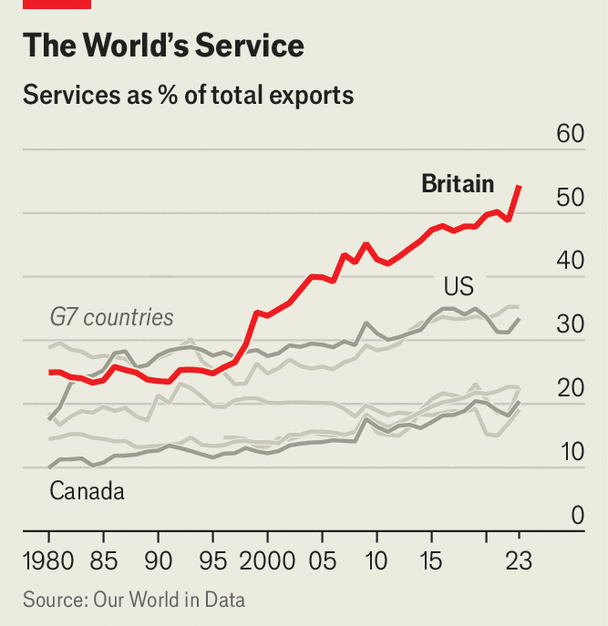

If there is one defining fact about the British economy, it is that services dominate. That, one could fairly reply, is true of every advanced economy, no matter the hopes of the manufacturing nostalgics. But the skew to services in Britain is remarkable, even compared with its peers. No other G7 country has services made up much more than a third of total exports. In Britain, that figure is over half.

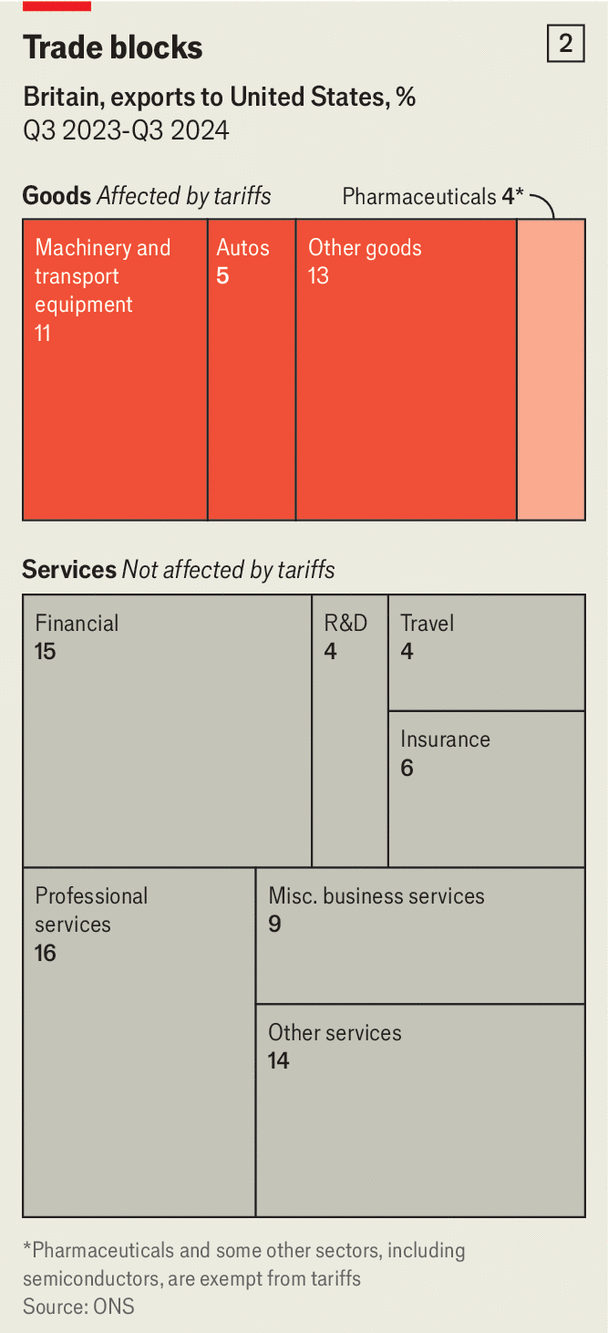

That trade comes mostly in the dull, professional sectors you’d expect: banking, law, insurance and the like. Naturally, un-bylined articles about the economy comprise a small but vital slice thereof.

When tariffs started raining down, that tilt offered an under-appreciated advantage: Donald Trump doesn’t seem to believe in services and has largely exempted them from his trade war. Both of the charts above come from a piece of mine from last April, explaining why Britain was well-insulated from tariffs as a result3.

The same cannot be said for the impacts of AI. Here, instead, the shape of Britain’s economy leaves it vulnerable. Take a look at the chart below, which slices similar data in a slightly different way: looking at the share of Britain’s total output that is services exports—about a fifth, triple the share of 30 years ago4.

Expensively slinging emails across the Atlantic surely ranks high on the list of tasks that firms are already looking to automate. And when firms abroad do that automation, the productivity gains land entirely elsewhere (New York, say); Britain loses out.

2. Rising returns to dynamism

A fair riposte would be to say that this downbeat framing is not inevitable. British companies, after all, could use AI to turbo-charge their own offerings, boosting productivity at home and competitiveness abroad. If Britain’s advantage in legacy professional services persisted (and perhaps grew) through the internet era, why shouldn’t the same go for AI?

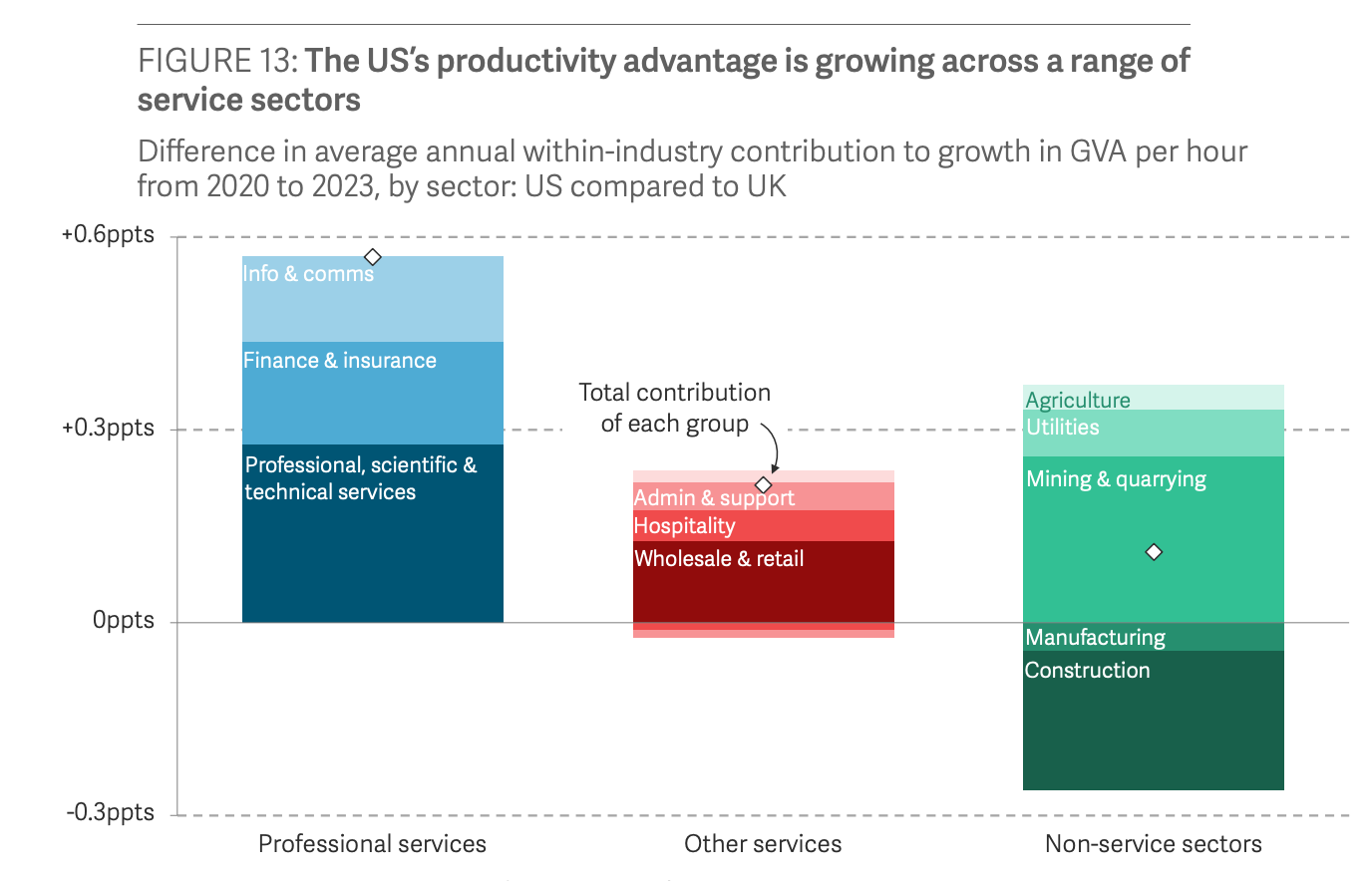

I’d argue the opposite claim is more compelling: that Britain’s economy is becoming less dynamic, exactly when dynamism is becoming more critical. The faster the world is changing, the greater the gains for the agile—and the perils for the sluggish. Take a look at the past few years. There are plenty of explanations jostling about for America’s recent outperformance. Certainly, Europe’s natural gas shock in 2022-3 didn’t help things. But if I had to pick one factor5, I’d probably go with B2B SaaS6. That is, the effective deployment of technology in unsexy sectors across the economy, what the Resolution Foundation calls (in a great and under-discussed report from last year comparing growth in Britain and America) “tech-using, rather than tech-producing services”.

I remember laughing when, during the late 2010s, a college friend interning at Goldman Sachs told me that the internal slogan of the day was “Goldman is a tech company”. Now, I rather think the bankers had a point. Or (to blow one of my own grievances out into an economic microcosm) just compare the quality of the United or Delta apps to the buggy mess on offer from BA.

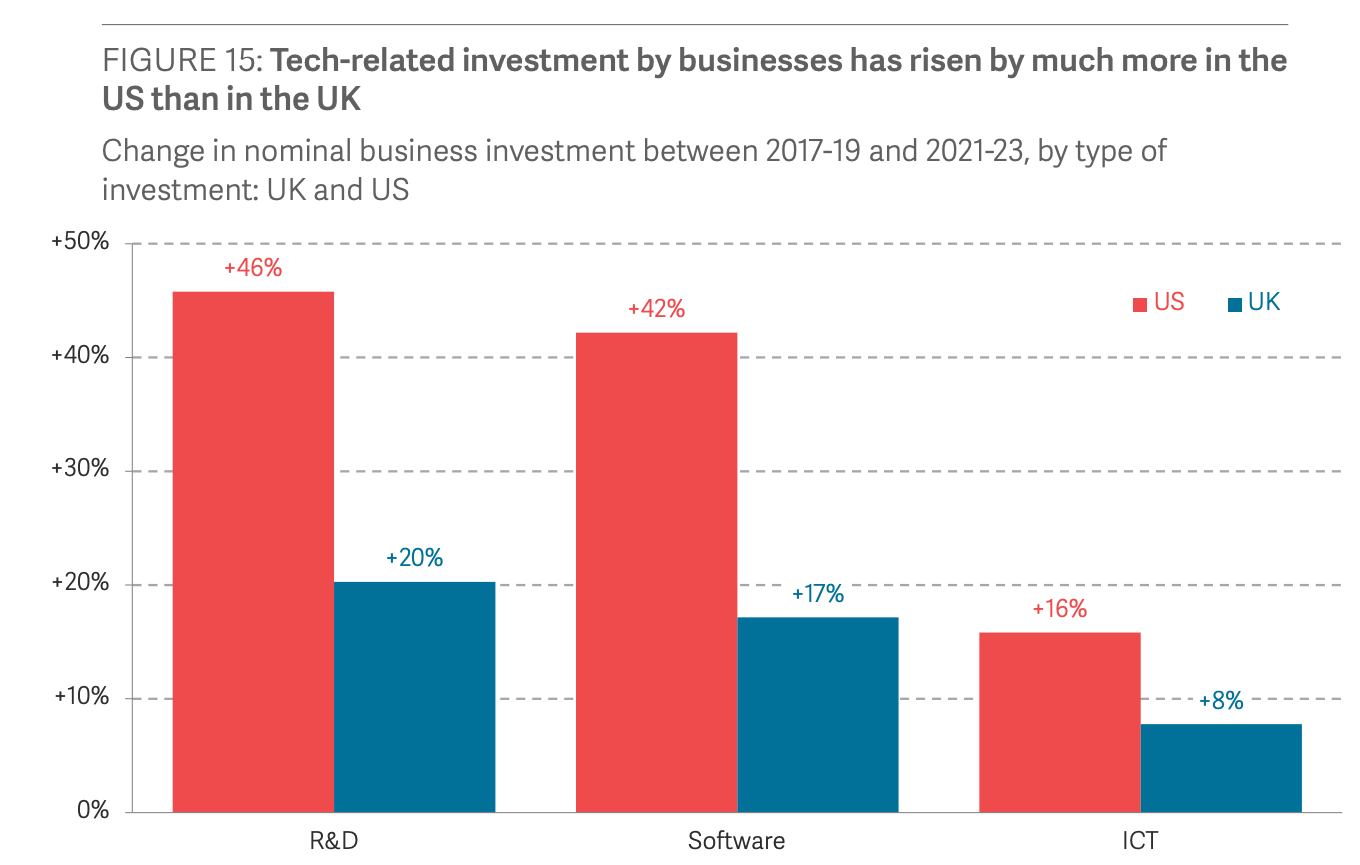

You can see all that in the two charts below. Already, the core drivers of American outperformance compared to Britain (and, indeed, most of Europe and the Anglosphere) are in the high-end services that Britain thinks it excels in. Already, investment growth in tech and software has been twice as high in America. And, much as I grudgingly respect the Salesforces, Zooms and Workdays of the world, these figures come from a pre-ChatGPT period when the technology on offer was much less impressive than what we have now, and the returns from taking it seriously correspondingly much lower.

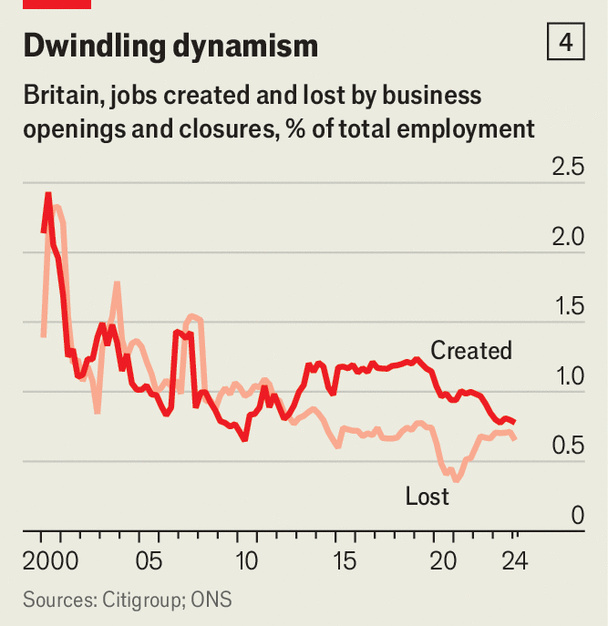

Tack that on to a longer trend, too, of declining dynamism across the British economy, which has been played out for decades. The next two charts measure that fall in two different ways. The first, which I published in June 2024 (for a cover arguing, in hindsight not unfairly, that Labour’s growth agenda was all-leaf-and-no-carrot), shows that fewer businesses are being born and, probably more important, fewer are dying.

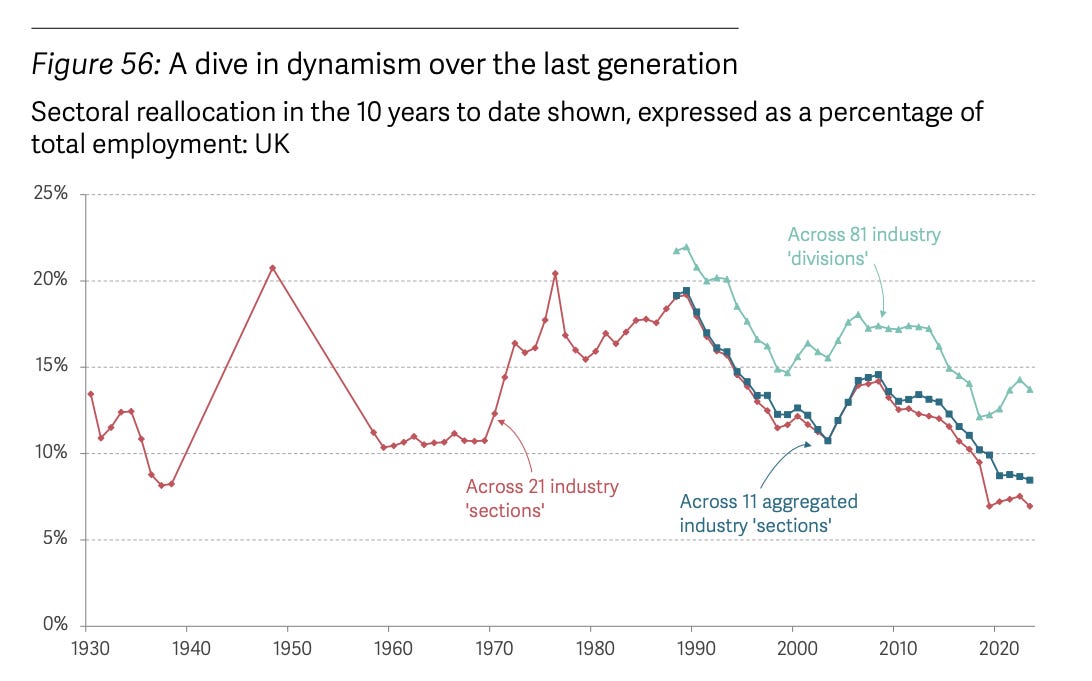

And the second, cribbed again from the Resolution Foundation, shows something similar over a longer timeframe: people are ever less likely to switch industry. A churning, fast-growing, competitive, dynamic economy should not have seen sector-hopping drop by half in twenty years.

In AI terms, that backdrop puts Britain in a double-vice: on one side, incumbents adopt new technology sluggishly (and slower than international peers—against whom they compete in the export market); on the other, not enough new competitors spring up to beat them. Britain’s consultants and lawyers of tomorrow could look like the European carmakers of today, crouching behind trade barriers while faster-moving foreign competitors use new (here, electric) tech to build a better and cheaper product.

One more cause for angst: labour regulation. An advantage that Britain has long held, especially compared to mainland Europe, is a fairly flexible jobs market7. The government is working to change that. I’ve stolen the charts below from a great piece by my colleague Matthew Holehouse. At exactly the wrong time, the Employment Rights Act will make Britain’s jobs market less competitive and more European (on labour policy, that is seldom a compliment).

3. Hoarders, not investors

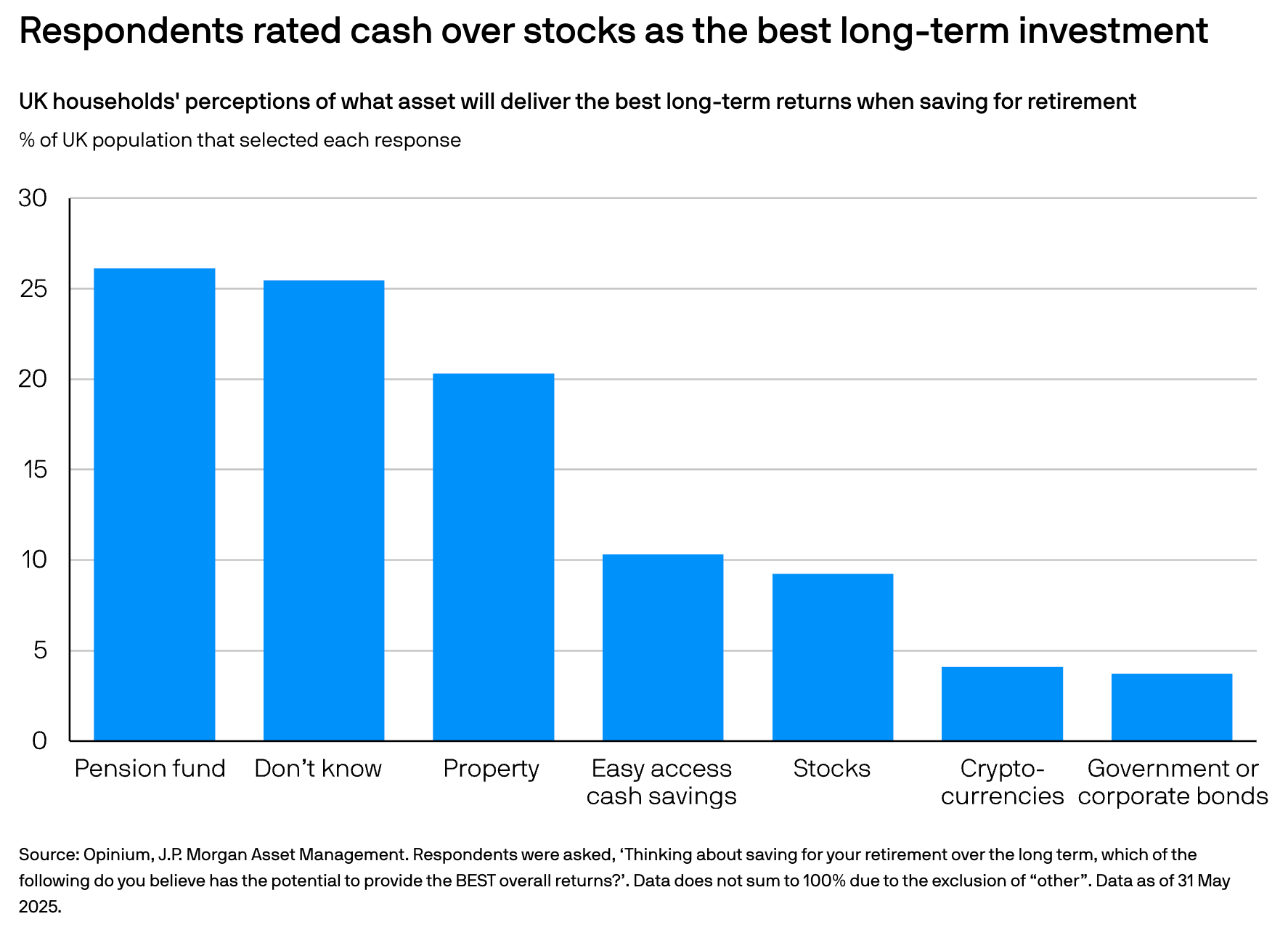

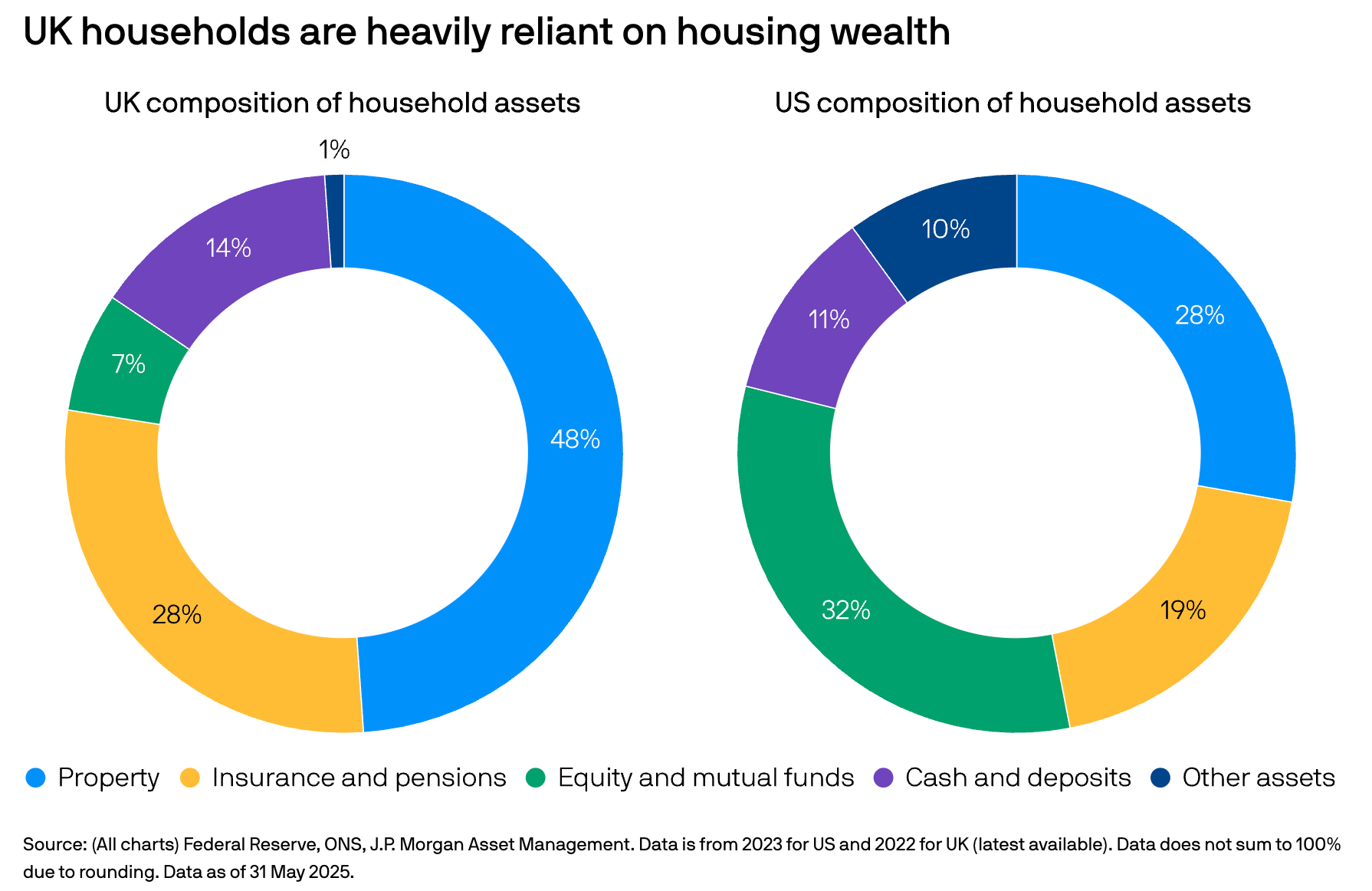

So Britain’s firms may well struggle to navigate AI. Troublingly, the same goes for Brits themselves. British households stand out internationally for holding lots of savings in cash, property and pension schemes (themselves often in low-risk fixed-income assets).

Conversely, British portfolios tend to be lighter on stocks. Happily, what equities British households do hold tend to lean more global than peers elsewhere (though successive governments have tried cooking up ill-conceived schemes to change that8.)

Contra their reputation as risky assets, a basket of stocks is probably (not investment advice!) just about the best thing to hold if the world turns upside down. Last week, I was reading “Wealth, War and Wisdom” by Barton Biggs, a Morgan Stanley strategist. He traces how financial markets responded to the Second World War. Then, inflation and financial repression made cash and bonds a poor bet. For pure wealth preservation, land was a good call (or a Swiss bank account). But over the long run, it’s hard to do better than simply having a stake in a slice of the real economy, which is what equities offer9. Even in countries ravaged by Nazi occupation, over a multi-decade timeframe stocks did very well.

What does that mean in an AI boom? To Biggs’s point, equities work well as a chaos hedge. Otherwise, almost certainly, real interest rates go up10, tracking a rise in productivity growth. So holding bonds (prices fall as yields rise) is not a great idea. Cash or land, especially near economic centres, probably does OK. Stocks in industries disrupted by AI might take a hit. For most others, their value might be crimped a bit by higher interest rates (knocking down the present value of future earnings), but that will almost certainly be swamped by the offsetting earnings boost from a productivity boom. Stocks in sectors poised to benefit from the AI productivity uplift, or selling bottlenecks to AI deployment, should do phenomenally well.

Compare that to the average Brit’s portfolio, and you see something pretty poorly-structured for this future: lots of cash and property, and (via pensions) fixed income. Not only might Britain’s economy lag if AI starts to seriously matter, but its wealth could too.

4. All R, no G

An AI boom could also have worrying implications for government debt. (I’ve stolen this observation from Luis Garicano, which he applied to mainland Europe. But Britain would face the same issues.) What happens if an AI boom raises global interest rates, but doesn’t correspondingly raise productivity everywhere?

Global bond markets are highly correlated, and becoming more so, as the chart below shows. If the yields on US treasuries soar, Britain and Europe won’t be spared. That has fairly nasty implications for governments’ ability to service their already-hefty debt loads. Then, failure to adapt to AI wouldn’t just mean a relative loss of competitiveness, but an outright decay in laggard countries’ public finances.

The broader macroeconomic ripples would be unpleasant, too. Playing out the full scenario gets rather fiddly, but an AI-led cycle that raises global yields could well also impose inappropriately high long-term interest rates on laggard economies, constricting access to credit. There is a halfway-parallel to the 1990s-era anxieties about America damaging emerging markets by exporting its monetary cycle: less about importing capital flows and currency crashes—more getting stuck with other countries’ interest rate environment while lacking their growth.

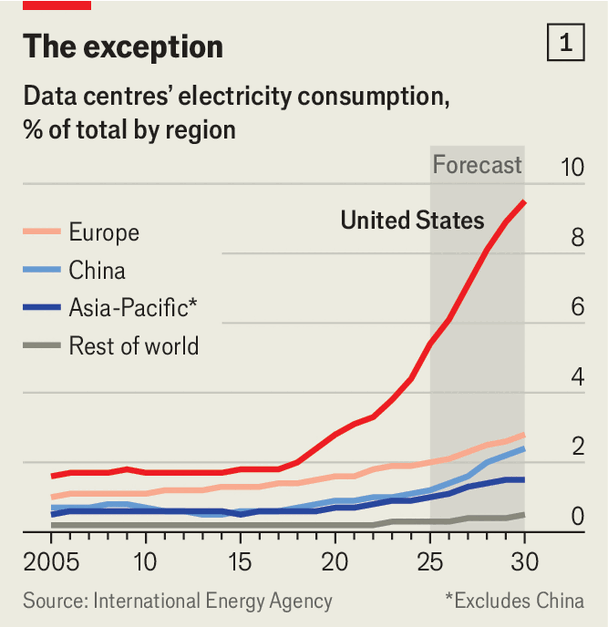

5. A net compute importer

Living in Washington, conversations about data centres are just about inescapable. (I can heartily concur with my friend Jasmine Sun’s observation from her expedition here a few weeks back: “People are truly, truly obsessed with data centers”.) Warehouses of chips are mushrooming up just about everywhere, gobbling up power, spurred by ever-higher estimates of compute needs. Big tech is now doing more capital investment than the entire oil and gas industry.

Back in London, data centres come up rather less frequently. Expensive energy and the usual tale of onerous land-use rules has muffled the data centre boom in Britain. Britain is missing out on a wave of foreign investment, in the aspect of the AI revolution that (so far) has had by far the clearest macroeconomic impact. Another AI loss to chalk up.

And here’s another concerning parallel. 15 years ago, the shale gas revolution looked a bit like the data centre one: a new technology suddenly, and quickly, sprouted up in physical form. In America, that led to energy independence and—in a roundabout way—granted a freer hand to sanction Russia after its invasion of Ukraine, or (for better or worse) attack Iran this week. Britain and most of Europe, meanwhile, have been bogged down by their failure to adapt and stuck paying through the nose to import gas. (France, with its nuclear fleet, is a notable exception.)

Being a net importer of a core commodity in the modern economy is seldom an excellent place to be, even if global markets are deep and liquid as they are for energy. Perhaps, compute will be so overbuilt and so cheap that this won’t matter. But it pays to be cautious. We don’t know yet whether the profits from AI advancement will land mostly with model-builders, compute-providers, the companies actually deploying the technology, or some jumble of all three. We do know that net energy importers haven’t had a great time of things in the 2020s. What will being a net intelligence importer look like in the 2030s?

6. The two cultures

Last, never let it be said that there is anything wrong with people mostly trained in essay-writing dabbling in coding and chart-making. (I’d never dream of talking myself out of a job.) But Britain does, long-standingly, have an elite class rather light on scientists, or on those who take scientific knowledge seriously. This is best elucidated in The Two Cultures And the Scientific Revolution, a lecture given by the novelist and chemist CP Snow in 1959, as the atomic age beckoned:

“But I believe the pole of total incomprehension of science radiates its influence on all the rest. That total incomprehension gives, much more pervasively than we realise, living in it, an unscientific flavour to the whole ‘traditional’ culture, and that unscientific flavour is often, much more than we admit, on the point of turning anti-scientific. The feelings of one pole become the anti-feelings of the other. If the scientists have the future in their bones, then the traditional culture responds by wishing the future did not exist. It is the traditional culture, to an extent remarkably little diminished by the emergence of the scientific one, which manages the western world. This polarisation is sheer loss to us all.”

Plenty of countries reckon with this anxiety. America’s congressional hearings on social media or AI, where octogenarian House representatives quiz Silicon Valley executives, are frequently excruciating. Dan Wang unflatteringly compares America’s “lawyerly society” to China’s “engineering state”.

But, Britain today has an especially bad dose (as it did in Snow’s day). Probably the clearest way to see the issue is less in amateur sociology, and more in outcomes. Britain, in large part as a consequence of that elite skew, does not seem to excel at tech regulation. See the failed efforts by the Home Office to persuade Apple to put a backdoor into its products. Or the mess of over-zealous policing of online speech. Or the chaotic rollout of the Online Safety Act.

The policy dilemmas that AI does, and will, raise won’t be easy—and I know and respect a number of people in and out of government in Britain who are thinking about them. But getting the policy response right will mean swimming against the stream of the knee-jerk technophobia of Britain’s political culture.

To be honest, one danger I’ve been quite conscious of in writing this piece is using AI as an excuse to argue for things that I believe in anyway. Had large language models never been invented, I’d still doubtless be banging on about Britain’s problems with business dynamism or how high energy prices were crimping the economy. Plenty of the issues blocking data centres apply to all sorts of other infrastructure, and have for decades.

So let me close by trying to zero in on something more specific. The single strongest temptation as AI disruption intensifies will be to lock things in place and buy time to think. Slow-walk the rollout of self-driving, so taxi and lorry drivers aren’t out of a job; clog up AI adoption in law or accounting with licensing schemes and regulations.

That impulse is understandable, and the political pressure to lean that way will be vast. There will be obvious precedent in the Covid furlough scheme, which was (I’d argue—though I’ll leave it to another post to justify that conclusion) an economic disaster, but briefly made Rishi Sunak the most popular politician in the country.

Repeating that playbook would be a serious mistake. Unlike Covid, there is no rowing back on AI. Other countries will be moving faster, and happily gobble up Britain’s market share. I hope Britain doesn’t let them.

Though, in the interests of accurately accounting for past predictions, I struck a more sanguine note in my last Economist cover on Britain, in July—arguing (as an aside in a leader on “Bargain Britain”) that Britain was well-hedged for an AI upswing by virtue of its strong domestic tech industry. I’m still a fan of the broader thesis of that cover, but am now gloomier on the AI-specific side. (I think I over-weighted the importance of an AI industry and under-weighted the importance of the rest of the economy being in a position to adapt.)

My colleague Georgia Banjo wrote a good piece on AISI recently.

That argument has held up decently well, I think. Though it is a little hard to tell, since the global impact of tariffs across the board has been far less than was then feared. Since I’ve pulled the charts straight from that article, the specific values are a year or so out of date. But these series tend to move slowly, so won’t look all that different today.

As an aside, the “goods” line on that chart chronicles its own disaster—the impact of hard Brexit and high industrial energy prices.

The answer here does rather depend on the timeframe. Over a longer timescale, I’d put physical-environment blockers like housing, energy and transport higher on the list.

Business-to-business software as a service. About the hottest sector in public and private markets, until a month or two ago when the market started pricing the risk of AI-related disruption and (more saliently, I think) margin compression.

Read Pieter Garicano in Works in Progress for why that European model is so destructive to innovation.

The main exception to this was countries that went Communist after the war. There, holding equities was inadvisable, though so were most assets. A lucky few landowners (or their descendants) managed to recover pieces of their former holdings after Eastern Europe went capitalist in the 1990s.

One interesting wrinkle in that view is that, through 2024, big model releases appear to have been associated with declines, not rises, in interest rates. At some point I may try to extend that paper and see whether we see the same for more recent advances.

Brilliant (if depressing) piece.

A thoughtful and balanced post. Would like to see the employment data (when available) regarding starter positions within the UK service sector. I suspect the impact of AI will feature in the next UK election (but in typical British fashion we won’t want to discuss the full implications lest it frighten the horses).